Introduction

When purchasing a new vehicle, one of the essential considerations is insurance. While standard auto insurance covers damages and liability, it may not always be enough. This is where GAP insurance comes into play. GAP (Guaranteed Asset Protection) insurance is a crucial policy that protects car owners from financial loss in case of a total loss or theft. In this article, we will explore GAP insurance in detail, its benefits, how it works, and whether you need it.

What is GAP Insurance?

GAP insurance is a type of auto insurance that covers the difference between the actual cash value (ACV) of your car and the amount you owe on your car loan or lease. If your vehicle is stolen or declared a total loss due to an accident, standard car insurance only reimburses you for its depreciated value. This can leave a financial gap if you owe more than the car’s worth. GAP insurance helps bridge this gap, ensuring you don’t have to pay out-of-pocket for the remaining loan balance.

How Does GAP Insurance Work?

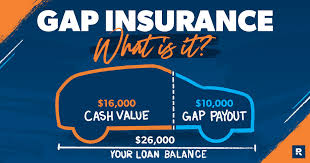

When you purchase a new car, its value starts depreciating as soon as you drive it off the lot. If your car gets totaled within the first few years, its market value might be significantly lower than what you owe to the lender. Here’s how GAP insurance works:

- You buy a car for $30,000.

- After one year, its market value drops to $24,000.

- You still owe $27,000 on your loan.

- If your car gets totaled, standard insurance pays only $24,000.

- GAP insurance covers the remaining $3,000 so you don’t have to pay it yourself.

Who Needs GAP Insurance?

While GAP insurance isn’t mandatory, it is highly recommended in the following cases:

- If you financed your car with a small down payment (less than 20%).

- If you have a long-term loan (60 months or more).

- If you leased your vehicle (as some lease contracts require GAP insurance).

- If your car depreciates quickly (luxury or high-end models tend to lose value faster).

- If you rolled over negative equity from a previous loan into your new car loan.

Benefits of GAP Insurance

GAP insurance offers several benefits, including:

- Financial Protection – Prevents you from paying out-of-pocket for a totaled vehicle.

- Peace of Mind – Reduces stress in case of an accident or theft.

- Affordable Cost – Typically inexpensive compared to other insurance add-ons.

- Covers Loan Balance – Ensures you don’t owe money on a car you no longer have.

Where Can You Buy GAP Insurance?

There are multiple ways to purchase GAP insurance:

- From Your Car Dealership – Often included in finance or lease agreements.

- Through Your Auto Insurance Provider – Some insurers offer GAP insurance as an add-on.

- From a Third-Party Provider – Independent insurance companies may provide more competitive rates.

How Much Does GAP Insurance Cost?

The cost of GAP insurance varies based on the provider and vehicle price. On average:

- From a dealership: $400 – $700 (one-time fee)

- From an insurance company: $20 – $40 per year

- From third-party providers: Varies but can be more affordable

How to File a GAP Insurance Claim

If your vehicle is totaled or stolen, follow these steps to file a GAP insurance claim:

- Report the incident to your primary auto insurance provider.

- Obtain a settlement letter stating the actual cash value of the car.

- Contact your GAP insurance provider with the necessary documents.

- Submit loan payoff information from your lender.

- Receive compensation to cover the difference.

Common Misconceptions About GAP Insurance

1. “GAP Insurance Covers Everything”

GAP insurance only covers the difference between your car’s value and the remaining loan. It doesn’t cover repairs, maintenance, or new car purchases.

2. “All Vehicles Need GAP Insurance”

Not everyone needs GAP insurance. If you own your car outright or your loan balance is lower than your car’s value, GAP insurance may not be necessary.

3. “GAP Insurance is Expensive”

Many people assume GAP insurance is costly, but in reality, it is quite affordable compared to the potential financial risk of not having it.

FAQs About GAP Insurance

1. Is GAP Insurance Required by Law?

No, GAP insurance is not legally required, but some lenders may require it for financing or leasing agreements.

2. Can I Cancel GAP Insurance?

Yes, most providers allow cancellation, and you may be eligible for a refund if canceled early.

3. Does GAP Insurance Cover Deductibles?

Some policies cover deductibles, but it depends on your insurance provider.

4. How Long Do I Need GAP Insurance?

You should keep GAP insurance until your car loan balance is lower than the vehicle’s actual value.

5. Can I Transfer GAP Insurance to a New Car?

No, GAP insurance is tied to a specific loan and vehicle. You’ll need a new policy for a new car.

Conclusion

GAP insurance is a valuable financial safeguard for car owners who owe more on their loan than their car’s worth. While it may not be necessary for everyone, it provides peace of mind and financial security in case of an accident or theft. Before purchasing GAP insurance, evaluate your loan terms, car depreciation rate, and insurance options to make an informed decision. If you’re financing or leasing a vehicle, GAP insurance might be a smart investment to protect yourself from unexpected financial burdens.